This reinforces the overall view that the reinsurance sector is being hit harder this year than by the 2020 catastrophe losses, and even more so the retro market.

Initial expectations for the Ida market loss were closer to the $20bn-$25bn range, with various initial picks still in the teens, but since then the market is now adding on roughly $3bn-$5bn for private flood losses from Ida’s Northeast deluge.

Combined with general fears over how complex and long-winded the claims adjustment process for the hurricane could be, more sources were now reckoning on Ida costing $25bn-$35bn, with a bias towards the $30bn+ range.

Getting into these $30bn+ levels would begin to pull into play more occurrence retro coverages, sources noted.

The aggregate retro market – which provides perhaps $4bn to $5bn of up to $20bn total retro XoL limit – was already expected to be in for another challenging year, as Ida is the third major loss of 2021 alongside the escalating European Bernd flooding and Winter Storm Uri.

Sources suggested that collateral trapping would be quite extensive – estimates ranged from 50% to 80% of limits – and that the real question was not that trapping would be a problem, but how much would ultimately be lost within the aggregate market. Some said there was potential for losses to reach up to 50% of limits if Ida reaches the top end of projected losses.

Within the occurrence market, estimates also ranged widely, from 10%-25% of limit potentially exposed to Ida claims. Specific deals will vary, but generally occurrence triggers start kicking in around the $20bn industry loss mark, with typical exhaustion points designed to run up to roughly the $70bn mark, a source explained.

Much more occurrence retro limit was written on rated paper for 2021 than in past years, so this will make trapping less of an acute issue ahead of renewals. However, it will complicate negotiations for the fronting reinsurers where they are sharing this risk with new capital providers.

On the ILW market, $30bn also marks a common trigger point, with a lot of deals traded around the $30bn-$35bn range. However, one complicating factor for this segment is that the overall Ida loss estimates being discussed include components of claims that are not covered by PCS estimates, such as offshore claims, or where claims are harder to track, such as commercial losses. Hence, there was a general expectation that the PCS loss estimates would initially come in much lower than the $30bn+ figures now being discussed.

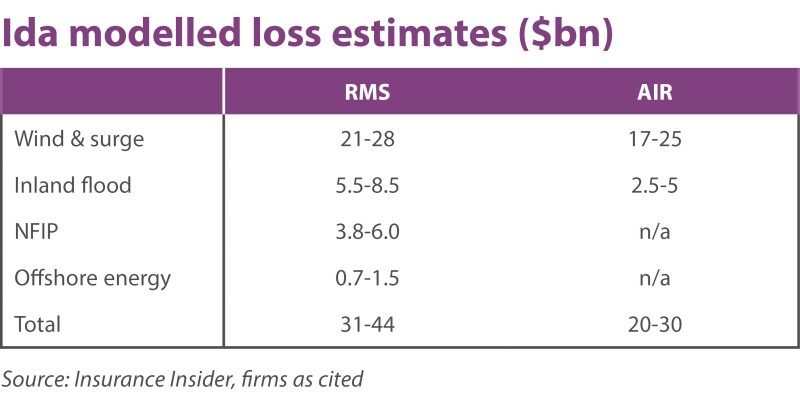

Modelling firm RMS has put the highest range estimate on the storm to date at $31bn to $44bn, but this includes up to $6bn of public National Flood Insurance Program losses, versus AIR’s onshore private losses of $20bn-$30bn.

“No story to sell”

Moreover, while post-pandemic 2020 fundraising brought significant fresh capital into the retro market, through deals such as the PartnerRe sidecar, and new carrier Acacia, it remains to be seen how capital providers respond to another aggregate retro loss year.

In general, on the ILS side more investor interest this year has been geared towards the remote risk end of the spectrum. And for the different types of investors participating in the higher-risk spectrum, 2021 could bring a third year of significant loss activity in the past five years, after the major write-downs in 2017 and 2018, and noise around BI trapping issues in 2020.

Unlike last year’s more buoyant post-pandemic market, in 2021 there is “no story to sell”, one ILS manager observed. “The vibe is different,” they added, noting that there was relatively subdued talk about rate increases given strong capacity across the rated market. Another broking source agreed, saying that they saw little interest and demand from the investor community in the sector given climate change concerns.

Exacerbating factors

Ida initially looked like a standard wind loss, albeit with the added complication of hitting during a pandemic. But it now looks less like a vanilla claims event, with the Northeast flooding damage set to complicate the assessment process.

Moreover in the south, slow-moving storm Nicholas also dumped large amounts of rainfall on Louisiana and Texas within a couple of weeks of Ida. This will exacerbate claims in Louisiana, and where tarped properties experience extra mould or water damage, these additional costs would likely be put onto Ida claims as the proximate cause.

Despite some promising signs, with power returning to most of New Orleans within a week of the storm, pandemic supply chain disruptions and the difficulty in accessing damaged areas in Louisiana have made information hard to come by.

Nat-cat reinsurers hit harder by 2021

The run-up to the key January renewals for the reinsurance market is just beginning.

But it is already evident that 2021 is having a much harder impact on catastrophe reinsurers than 2020, notwithstanding last year’s record-breaking hurricane season.

Many of last year’s storms resulted in retention hits for insurers, and while regional carriers might have hit reinsurers with first- and second-layer losses, even Hurricane Laura failed to trigger some major nationwide programmes.

Meanwhile, the European business interruption losses were a major driver of overall Covid claims, but they fell more heavily on a narrower group of carriers compared to the distribution of US losses, with less retro relevance.

In contrast, for this year’s events, a higher share of Ida and Bernd losses at least are being transferred straight to reinsurers.

Allstate, for example, already said it would transfer more than half its $1.4bn gross Ida losses to reinsurers.

As a rough benchmark, the premium attached to the global nat-cat XoL market is somewhere around $20bn.

One senior underwriter expected that around $16bn-$17bn of Ida losses would go to reinsurers, in line with the upper end of another source’s estimate that a third to half of the loss would be reinsured.

The European flood losses are expected to be even more heavily reinsured; with Bernd losses now expected to total almost $12bn, these two sources expected somewhere between $5bn to $8bn to be picked up by reinsurers.

If half of Uri’s potential $15bn losses flowed to reinsurers, this would put the cat XoL market at roughly a 150% loss ratio, the underwriter noted.

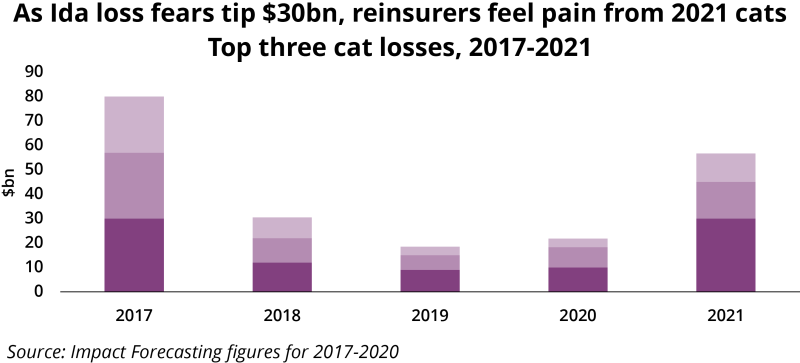

Looking at the top three nat-cat losses for each of the past five years, it is clear that 2021 has brought larger scale events that trail only 2017 and that are more likely to have made a bigger dent on reinsurers.

Even within the major loss year of 2018, the top three events according to contemporary estimates from Aon’s Impact Forecasting only cost just over $30bn altogether (although significant Irma creep was recognised that year).

With Swiss Re putting total H1 2021 cat loss activity, including minor perils that may not have impacted reinsurers, at the second highest H1 level on record at $42bn, the rest of the hurricane season will be critical for cat reinsurers.

Bernd and Ida will already have taken the H1 tally much further on from this $42bn figure – putting a $100bn loss year within reach if another moderate loss arises. This would be the third such year by Sigma records after 2011 and 2017 – and one that comes after the market has been gradually worn down by multiple years of poor performance and post-event disappointments.