Business interruption

-

The firm reported record fee income of $128.2mn in 2024, up 26%.

The firm reported record fee income of $128.2mn in 2024, up 26%. -

Novelty premiums will likely fade once investors are more comfortable with the risk.

-

The company said $13bn-$22bn will come from wind damage.

-

Earlier this week, RMS estimated insured losses for Helene and Milton at $35bn-$55bn.

-

The figure does not include NFIP losses.

-

Most of the estimated insured losses will be retained by insurers.

-

Building better exposure datasets could draw a broader range of investors.

-

The carrier estimates the total industry loss for the Microsoft/CrowdStrike outage at around $1bn-$2bn.

-

The event could unpack issues around accumulation risk and cloud services.

-

The biggest losses were from wind damage after the storm’s Texas landfall.

-

CFO Dacey said ILS investors were not extrapolating too much emphasis from strong returns in 2023.

-

The Magnitude-7.4 earthquake occurred early on 3 April.

-

Revenue, country and industry sector drive modelled output divergence.

-

The carriers were in arbitration with UnipolRe and Gen Re.

-

More than three-quarters of local exposure is ceded to highly rated reinsurers through excess of loss protection, according to the rating agency.

-

In a presentation before Florida lawmakers, Cerio noted recent success in Citizens’ efforts to move policyholders to private insurers and reduce risk exposure.

-

The carrier describes reinsurers’ current strategy of dealing with cyber policies as "a game of whack-a-mole"

-

The ILS business ‘continues to be an important differentiator’, says Aspen CEO Mark Cloutier

-

A Guy Carpenter report recently noted that risk models are converging for the most remote risk levels.

-

Softening cat bond rates are among the bearish signals for cat rates, but latent new demand and still-cautious supply should prolong reinsurer gains.

-

The insurer’s expected full-year combined ratio is 94% and constant currency GWP growth 10%.

-

The modeller also said that losses to the National Flood Insurance Program will likely remain under $300mn.

-

Lower-attaching Florida ILWs had been more in demand at this year’s mid-year renewals.

-

The broker said climate, conflict and capital concerns will keep driving up reinsurance rates but suggested new capital may be attracted to the market.

-

The carrier said its commercial business gave the company a platform to build on.

-

Experts say cyber ILS offerings including cat bonds could be near, but concerns over structures, modelling and correlation persist.

-

There is a tension between securing payback and negotiating higher retentions.

-

The insurer predicts there will be some release from its provision, but it will happen over time and is subject to court proceedings.

-

Policy holders The Taphouse Townsville and LCA Marrickville, and insurer IAG have each filed applications for special leave to appeal to the Australian High Court.

-

Even though underlying ILS market conditions are improving, getting a hearing from investors could become harder.

-

The court upheld decisions made in October, although it reversed some elements of the case between IAG and Meridian Travel.

-

Investors are increasingly concerned about legislative changes and climate change, but there are drivers for optimism, the consultant said.

-

Another pandemic outbreak came in fourth place, with 22% of respondents saying they were worried about further health and workforce issues and movement restrictions in 2022.

-

Personnel turnover and ongoing redevelopment into new areas were the notable themes of the past 12 months.

-

October storms touched the insurer’s occurrence reinsurance trigger of A$169mn.

-

Sidecars have lost some of their lustre in recent years but are still generally seen as an efficient diversifier.

-

The judgment ruled that clauses in insurers’ BI policies covering infectious diseases meant cover was only present for closures relating to an outbreak on assureds’ premises specially.

-

Surpassing the $30bn threshold will trigger more occurrence covers, as another painful year looms for aggregate writers.

-

The updated loss estimates come on top of the $14bn to $19bn industry loss range the analytics firm provided last week.

-

The cat risk modeller’s estimate is well ahead of KCC’s $18bn, as RMS said infrastructure in the states impacted by Ida have “never experienced such a strong hurricane wind intensity”.

-

The broker expects ongoing single-digit growth within the ILS market.

-

Post-Covid demand surge is a particular focus and fear.

-

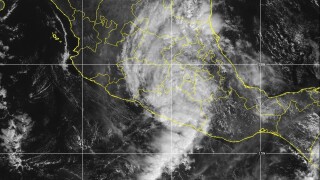

Ida has weakened to a tropical storm after knocking out power to New Orleans and other coastal areas of Louisiana overnight.

-

The carrier said July flooding in Europe and South African unrest would bring losses in the mid-triple-digit million range for Q3.

-

The company grew P&C net written premiums by 47%, while the non-life combined ratio improved 32 points to 89% during the second quarter.

-

RMS model update points to ‘fairly large’ rise in hurricane losses for US Northeast and Mid-AtlanticThe RMS V21 model update for North Atlantic hurricane incorporated data from recent major loss years but overall annual average losses have only risen up to 10% across the US.

-

The November gathering will aim to combine a virtual segment and a “scaled-down” live event held in line with health and safety protocols.

-

There is little sign of retro demand returning after buyers cut back in January.

-

The carrier last year said its K sidecar would pick up Covid claims over time.

-

The reinsurer’s net exposure was up 36% as it retained more risk in retro and North American cat.

-

The firm reported an industry-wide loss of $36.8bn caused by the pandemic, up from $29.5bn in Q3.

-

Covid-19 losses remained stable as the insurer said rate rises should endure.

-

Interest in parametric coverages has increased among insurance buyers as a response to coverage gaps exposed by unanticipated losses and tightening traditional market capacity.

-

Private-public partnerships can provide first-step survival financing if not a full solution for all companies.

-

The tally so far comes in far below the broker’s year-ago estimate of $80bn for a twelve-month lockdown.

-

The organisers pledge to return to Monte Carlo in September 2022.

-

Aon has said it expects the economic cost of physical damage and business interruption caused by the polar vortex-linked cold snap to “well exceed $10bn”, in an Impact Forecasting report released on Thursday.

-

The firm reported a $100mn drop in ILS AuM to $1.4bn, although previously had said deployable capital was lower.

-

Some had argued that the definition of occurrence used by judges could make it harder for insurers to aggregate treaty claims.

-

The carrier revealed 10.9% premium volume growth at 1.1.

-

The fund’s worst ILS return to date is understood to be driven by investments hit by Covid-19.

-

Some pointed to low average costs to fix burst pipe claims, while others warned that BI could drive up losses.

-

The EU’s chief insurance supervisor wants capital markets to augment the capacity provided by traditional (re)insurers.

-

The European (re)insurance supervisor said correlation to financial market risk made the idea a challenging one while reinsurance appetite is also very limited.

-

The Australian carrier has also modestly increased its reserves for Covid-19 BI claims.

-

The analyst predicts the insurance sector could experience its best performance in nearly a decade.

-

The ratings agency foresees no “material effect” on the capital or earnings of UK commercial property insurers following the Supreme Court ruling.

-

Fenchurch Law partner suggests "aggressive" initial claims adjustments will be unwound and the reinsurance context will need specific consideration.

-

The firm aims to use AI to fill the protection gap left by “black swan” events like Covid-19.

-

Some markets on the programme have pushed back on the inclusion of event cancellation exposures.

-

This came after analysts said reinsurers could face further cat losses as a result of the case, although XoL claims are likely to be disputed.

-

Citizens projected it would cede $94mn in storm losses to reinsurers but has cut this to $62mn.

-

The court’s decision was the final step in a protracted legal battle stretching back to May last year.

-

The year was marked by record North Atlantic storms, which put the loss tally more than 40% ahead of mild 2019 experience.

-

The newcomer held the same role at the French insurer’s London hub for around nine years.

-

Net assets have grown 5% year-on-year to $876mn as of 31 October 2020.

-

The consultancy said losses were expected to keep mounting following Q4 disclosures.

-

Losses were relatively evenly divided between the two events.

-

The insurer said its reserving was still adequate after the court supported its overall approach, but said biosecurity exclusions were not sufficient to decline claims.

-

The regulator says that the insurance sector had remained resilient this year but faced ongoing threats.

-

Occurrence retro rates are among the segments where rate pressure is abating, although the outlook remains somewhat opaque in a late renewal.

-

Carriers have raised $19bn so far this year, with another $3bn in the pipeline, the broker says.

-

ILS funds fell 0.03% in October according to the ILS Advisers index, after reaching a 2020 high point the previous month.

-

The German carrier pegs the full-year impact of the pandemic on its reinsurance operations at EUR3.4bn.

-

The carrier seeks to address potential BI liabilities following a court ruling.

-

A fresh BI ruling in Australia this week highlighted the industry's reason for caution over Covid exposure as legal actions continue.

-

-

The carrier plans to raise A$750mn in new equity capital to help shore up its balance sheet, and has further eroded its aggregate reinsurance.

-

Both Suncorp and QBE said multiple tests applied to trigger BI coverage, with QBE saying aggregate reinsurance should mitigate net exposure.

-

Court rules policy exclusions referring to outdated law not valid.

-

Australian carrier ups coronavirus BI provision to A$195mn.

-

The German carrier says P&C gross written premiums expanded 3% to $27.3bn in the period.

-

The carrier expects its total losses to reach EUR700mn-EUR900mn, as Covid claims reports begin to flow to reinsurers.

-

Sources think the court ruling in favour of a German beer hall in October could have widespread repercussions.

-

The carrier has fully eroded the retention on its group aggregate cover, limiting Q4 cat exposure.

-

The risk modelling firm also says offshore energy losses from the storm are unlikely to exceed $1bn.

-

More than 90% of crude oil production remained offline as of Sunday.

-

The case was launched after thousands of businesses attempted to claim on their insurance for Covid-19 related BI.

-

Applications have been filed for a 2 October hearing.

-

The president and CEO urges wordings precision to avoid cyber-related litigation.

-

If reinsurers prevail in limiting insurers from aggregating BI claims, this will shield retro markets.

-

The multidistrict litigation panel is expected to reach a decision by early next week.

-

Financial Services Director General John Berrigan wants to establish a new working group which will report back with proposals in the first quarter.

-

The latest estimate is marginally below a previously disclosed $75mn UK BI claims cap.

-

The Swiss carrier says any increase in P&C claims arising from the ruling won’t materially impact its earlier assessment of $750mn in Covid-19 claims.

-

The insurer could have total gross losses of more than EUR500mn, according to a French publication.

-

The estimate fell below the midpoint of Hiscox's prior modelled BI loss range.

-

Reinsurance recoveries and a drop in overall claims will offset the BI loss hike.

-

New capital could flow into the ILS sector if rates increase sufficiently, Fitch officials said.

-

It made a 4.4% gain over the past year from its insurance holdings, and has made 7.9% per annum since inception.

-

A New South Wales Supreme Court judge gives the go-ahead for the hearing to start on 2 October.

-

Nearly 1,000 insurance disputes over pandemic coverage were filed by the end of July, according to data highlighted by sister title Inside P&C.

-

The research firm says the pandemic will become the leading example of “silent” coverage uncertainty.

-

Earlier this month, we recapped some of the issues causing rising tensions in the retro market, where providers are pushing for release of capital trapped in connection to Covid-19 claims.

-

State Farm policies in question contain a virus exclusion, protecting the insurer from liability.

-

Accounting for expected H2 cat losses, the $500mn cover is only $20mn away from triggering.

-

The Australian carrier is also drawing down on other aggregate covers.

-

Lawyers are diligent in finding avenues to bring litigation against insurers, FedNat’s CEO Michael Braun told analysts on Thursday.

-

The UK insurer has exposure to BI losses through a Canadian dentistry book.

-

Axa estimated its total 2020 impact from Covid-19 for the group at EUR1.5bn, which it booked in the first half.

-

The retro vehicle has only picked up a small share so far but this will grow.

-

With the fundraising season approaching, tensions are rising over several points of dispute.

-

The law firm representing customer action groups claims brokers discouraged policyholders from lodging Covid-19 claims.

-

The judges will now consider their verdicts, with an ambition to produce a draft judgement in mid-September.

-

An unspecified superior court will hear the ICA-funded case, with the outcomes used by the Australian financial ombudsman.

-

The (re)insurance supervisor calls for “skin in the game” from all risk owners to reduce the risk of moral hazard arising from any state backstop.

-

The insurer also took a $400mn subrogation gain on wildfire losses.

-

In a joint defence, eight carriers in the High Court case reject FCA’s interpretation of proximate cause.

-

The regulator says that the losses were caused by a “jigsaw” of events that should be considered as a whole.

-

Insurance bodies including APCIA and NAMIC strongly oppose the draft legislation.

-

The carrier’s plan would provide up to $750bn in pandemic cover for small businesses and $400bn for large enterprises.

-

Property BI claims appear well below treaty reinsurance triggers.

-

The insurance industry's early victory could set a precedent for the many pandemic-related disputes in train.

-

The FCA test case for Covid BI claims could have huge implications for insurers.

-

To what extent does the business opportunity for new start-ups rely on BI losses that the industry is vigorously rebutting?

-

As many parts of the world start to emerge from lockdown, potential Covid-19 BI claims are yet to be tested.

-

A Hiscox group is seeking £52mn while lawyers for a QBE group action have secured funding.

-

The late July High Court hearing will also involve Arch, Argenta and QBE.

-

The risk of insurers having to make partial upfront payments up is likely to be highest in Continental Europe, Philip Kett adds.

-

The CIAB’s latest market survey also found carriers pushing for higher deductibles.

-

The insurer has a $75mn retention in place under its treaty.

-

The carrier has said it will appeal the court’s decision as it remains convinced the policy doesn’t cover such a claim.

-

The scheme could see claimants in different sectors offered pence per pound of limit purchased.

-

Voluntary insurance participation, backed by reinsurance, is a better alternative than a replica of the US terrorism backstop, they argued.

-

Collateralised re and sidecars are more likely to become subject to legal disputes around wording, the agency said.

-

The carrier is one of a few that offers affirmative BI cover.

-

The carrier’s P&C division could miss its 2020 operating profit target by 20 percent, CFO Giulio Terzariol said today.

-

Major cat reinsurance losses are unlikely without over-reaching judicial action, the HSCM Bermuda leader argued.

-

The “magnitude” of claims could ease in future quarters, Argo CEO Kevin Rehnberg said.

-

A judicial panel will decide whether federal cases should be combined into a single multi-district lawsuit.

-

The ILS market is among the leaders in holding firm on exclusions.

-

An analyst said the fundraise offered investors “a secure balance sheet” at an attractive valuation.

-

The insurer reserved an estimated £17mn for certain BI claims in Q1.

-

The carrier expects event cancellation losses from Covid-19 in the “mid-triple-digit-million euros”.

-

The new bill has a narrower scope than some previously proposed legislation, specifically targeting property, all risks and contingent BI policies.

-

Warren Buffett said the company faces a more limited impact from the virus than some other insurers.

-

Retro deals are seen as a particular concern over growing fears that trapped capital will again be an issue in 2021, as post-2017 innovations will be tested out.

-

Some believe US insureds could use the case to argue for BI coverage, but physical damage requirements are a strong defence for the industry.

-

The Covid-19 impact on Swiss Re year-end shareholders' equity was 1.63 percent and on Lancashire’s 2.9 percent.

-

The broker's total insured loss estimate spanned $11bn to $140bn, depending on the recovery from Covid-19.

-

The carrier’s P&C reinsurance business reserved $253mn for Covid-19 in the quarter.

-

The Markel co-CEO said the firm was warehousing retro risk until it raised capital for new platform Lodgepine.

-

Physical damage requirements should protect the carrier, it argued.

-

BI may seep into some reinsurance and retrocession covers but insurers will take the biggest hit, said the head of ILS at Schroders.

-

A trade body said the US legislation, if passed, would threaten the very existence of the business interruption insurance market.

-

More than 260 small businesses are reportedly taking action against the carrier.

-

About 75 percent of this figure is expected to come from BI losses.

-

The company previously pegged losses from the pandemic at between $20bn and $40bn.

-

Willis Re president Andrew Newman said capital will continue to flow into insurance if adequate returns are on offer.

-

The broker said Covid-19 industry claims should be manageable but the disaster makes a broader capacity squeeze more likely.

-

Reinsurance cover may be triggered and losses could end up significantly higher, estimates suggest.

-

The Starr CEO has hit back at moves to retroactively force insurers to accept coronavirus-related BI claims.

-

The insurer's Q1 net profit fell 25 percent to $600mn as cat losses were almost double those of Q1 2019.

-

The group aims to improve the industry’s resilience to future pandemics.

-

The decision comes as Lloyd’s and other insurers are named in a coronavirus class action lawsuit by restaurateurs and bar owners.

-

Founding partner of Twelve Capital Sandro Kriesch said he does not expect many ILS funds to “be on the hook” for Covid BI losses.

-

Greenberg defended the insurance sector and said it would be “unconstitutional” to retroactively rewrite contracts.

-

Early firm orders showed similar levels of increases to 2019, but are not expected to be a strong benchmark in a fast-changing market.

-

Chubb CEO says forced payouts would bankrupt insurers, while Allianz chief expects prolonged economic recovery.

-

The carrier said its reinsurance protection would respond to the loss, but recoveries may be limited.

-

Evan Greenberg is the only (re)insurance industry representative on the list of 200 executives who will advise on ending lockdowns.

-

The insurer highlighted its reinsurance cover in place as it downplayed the scope of BI exposure.

-

The regulator issued a notice after receiving complaints about insurers trying to dissuade policyholders from filing claims.

-

John Neal said losses would be significant, but not unmanageable.

-

The move highlights fears over pandemic exposure in Canadian property books.

-

Insurance capacity is limited for pandemics, said Swiss Re’s Edouard Schmid.

-

The Axa CEO said the initiative could be owned 50:50 by governments and private insurers.

-

Other US states have proposed similar legislation, as lawmakers explore options to keep businesses afloat.

-

Social inflation trends will make BI disputes particularly acute in the US.

-

Establishing federal backing would allow insurers to cede risk to central government.

-

Pre-Covid-19 mortality risks generally provided low single-digit returns, but significant repricing is underway.

-

The bill is similar to legislation that was proposed in New Jersey earlier this month and then pulled out of consideration.

-

Ohio and Massachusetts lawmakers propose re-writing business interruption policies to include coronavirus losses.

-

The backstop is just one of many ideas being floated, as governments and insurers look to improve preparedness.

-

The lawsuit will be a test case for property insurers holding that business interruption policies do not cover pandemic shutdowns.

-

The UK government agreed a pact with insurers, while the New Jersey State Assembly pulled a coronavirus-related bill.

-

The World Bank’s pandemic bond is expected to partially pay out as deaths surpass trigger points.

-

The UK terrorism insurance scheme looks to add additional layers to its main 1 March retrocession renewal.

-

The manager bought back and cancelled 900,000 ordinary shares worth $180,000 at the end of last week, as the process of winding up the business continues.

-

The Reinsurance Opportunities Fund also repurchased $43.4mn of shares in September.

-

Typhoon Faxai losses are unlikely to have a significant impact on the ILS markets, based on current industry estimates.

-

The risk modelling firm has released the highest estimate for industry losses so far and the top end of its prediction could hit some ILWs.

-

Widespread data theft from an email provider ranked as the most likely significant loss scenario in a report by the broker and analytics platform.

-

Chris Beazley’s role has been expanded to include head of reinsurance for MS Amlin after his departure.

-

The typhoon was the strongest storm to hit the Chinese province of Zhejiang since 2015.

-

Around half this total would be borne by the National Flood Insurance Program.

-

The UK state reinsurer completed the $50mn (£40mn) retro placement after the introduction of landmark legislation meant it could offer the cover for the first time.

-

The CEO of Aon Securities predicted that larger firms will continue growing at a faster rate than smaller counterparts.

-

Ten months on from Typhoon Jebi, there is still considerable uncertainty around why the storm’s insured losses are expected to be so much higher than the initial modelled figures.

-

Pool Re is likely to issue a new cat bond but will wait for volatility in the ILS market to settle down first, CEO Julian Enoizi said.

-

The CEO of Arch puts Jebi industry loss estimate at $13bn.

-

AIR's European storm insured losses estimates have been consistently more than those of their counterparts.

-

Former Marsh broker Richard Green has joined as regional head of the alternative risk transfer business.

-

The firm's latest figure for the storm is up from a $25.7bn estimate reported by this publication in June.

-

A previous estimate of $2bn to $4.5bn was released just prior to landfall.

-

Insured losses arising from Typhoon Mangkhut are expected to fall between $1bn-$2bn, risk modelling firm AIR Worldwide has said.

-

The city of Osaka sustained most of the losses.

-

AIR issued a range of $2.3bn-$4.5bn for the event which struck Japan on 4 September at the equivalent of a Catastrophe 3 hurricane.

-

The issue would be the ILS market’s first terrorism cat bond since the 2003 Golden Goal transaction.

-

ILS managers were offering larger line sizes and seeking to compete more often on reinstateable layers in the Florida June renewal, Willis Re observed in its mid-year 1st View report.

-

In its 1st View report the broker said the impetus for risk-adjusted rate increases had stalled at the June and July renewals.

-

Willis Re said global catastrophe pricing was broadly flat in an "uncontentious" April renewal, as it noted a dramatic change to the reinsurance landscape as primary carriers re-entered the market through M&A deals.

-

High initial loss estimates put out for Hurricane Maria by AIR Worldwide helped to fuel ILS fundraising that brought in more capital than would have otherwise entered the market, said panellists at an event hosted by sister publication The Insurance Insider last week.

-

The Bermuda Monetary Authority (BMA) has been criticised for demanding new disclosures from local alternative reinsurance operators without sufficient consultation with involved parties.

-

PCS has largely reversed an earlier cut to its loss forecast for Hurricane Irma, estimating the insured damage at $17.2bn, sister publication The Insurance Insider reported.

-

Insured losses for European winter storm Friederike will be between EUR1.2bn - EUR2.6bn ($1.71bn - $3.71bn), ranking it among the continent's most expensive storm losses, modelling firm AIR Worldwide has estimated today.

-

Allianz Risk Transfer (ART) has closed a second private cat bond covering weather at $14.5mn

-

Investment bank Jefferies said there remains a $20bn gap between (re)insurer loss estimates from Q3 catastrophe events and anticipated industry losses, as it predicted loss creep would fuel rate increases in 2018.

-

The October Californian wildfires would have a $90mn net negative impact on fourth quarter results at RenaissanceRe, the Bermudian carrier said today

-

Modelling firm AIR Worldwide has significantly revised its industry loss estimate for the October California wildfires to a range of $8bn to $10.5bn, up from an earlier $2bn-$3bn projection.

-

AM Best has said reinsurer profits could fall to a six-year low following catastrophes in the third quarter and that some companies may take up to three years to earn back losses.

-

Unreported losses from the third quarter catastrophe events should largely close the $70bn gap between disclosed claims and overall industry loss estimates, according to Morgan Stanley analysts

-

The $70bn gap between reported third quarter cat losses and industry loss estimates can be largely accounted for by (re)insurers and alternative markets that have not disclosed their losses, according to Morgan Stanley analysts

-

ILS can reduce the risk protection gap related to flood, according to co-head of ILS at JLT Rick Miller.

-

The recent wildfires that spread through California will lead to insured losses of $2bn to $3bn, AIR has said.

-

Modelling agency RMS has pegged losses from Hurricane Maria, the storm that devastated Puerto Rico earlier this month, at $15bn-$30bn

-

AIR Worldwide said that Hurricane Maria would cost insurers between $40bn-$85bn after devastating Caribbean islands from Dominica to Puerto Rico.

-

Risk modelling firm Karen Clark & Company (KCC) has estimated insured losses for the US and the Caribbean from Hurricane Irma at $25bn

-

The largest component of Harvey's damage will stem from flooding in the Houston area, so who is going to take those losses?

-

Fitch Ratings said that anticipated losses from the National Flood Insurance Program's (NFIP) $1bn reinsurance programme will be manageable for the carriers involved.

-

Hiscox reported an 11.2 percent year-on-year uplift in gross premiums written by its Hiscox Re and ILS division in the first half, as ILS assets under management reached $1.35bn.

-

Economic losses from a major cyber outage could be as large as damages caused by major hurricanes, according to a research report published by Lloyd's today.

-

The possibility of reinsurers jointly tapping into the ILS market was discussed at the inaugural International Forum for Terrorism Risk (Re)insurance Pools (IFTRIP) conference in Paris yesterday.

-

A second phase of the World Bank's Pandemic Emergency Financing Facility (PEF) should give premium reductions to countries that have invested in preparations to face a pandemic and also target the private sector, according to a new study

-

Insured losses from Tropical Cyclone Debbie have now hit A$660mn ($495mn), the Insurance Council of Australia (ICA) said in a statement today.

-

A reinsurance trading platform that is targeting up to a $1bn launch in 2018 begun its first simulation this month, with a group of 30-40 individuals from various ILS funds and reinsurance participants lined up to test the technology.

-

AIR Worldwide has said insured losses from the earthquake that struck New Zealand's South Island on 14 November could fall between NZ$1.15bn ($762mn) up to NZ$5.3bn ($3.5bn).

-

Swiss Re-backed Microinsurance Catastrophe Risk Organization (Micro) has launched a parametric catastrophe insurance policy in Guatemala designed for small businesses and farmers.

-

Hiscox Re reported a 27 percent jump in gross written premium (GWP) for the first three quarters of this year to reach $649.2mn, with its ILS business being a key driver of growth, Hiscox announced.

-

RMS has estimated US insured losses from Hurricane Matthew will fall between $1.5bn and $5bn, making it the costliest Atlantic hurricane for the (re)insurance industry since Sandy in 2012, but a far more modest hit than had initially been feared.

-

Insurers are preparing to pay out under business interruption (BI) policies in place to cover repairs to a production vessel owned by Tullow Oil, the company confirmed.

-

Cat bond upsizing climbed to new heights for the past year in the third quarter as the $925mn in final quarterly volume of public 144a ILS transactions came in at almost three times the $350mn originally targeted.

-

Markel Catco said August returns for the Catco Reinsurance Opportunities Fund would be impacted by a loss from the Jubilee oil field event totalling a 3.5 percent hit to net asset value (NAV).

-

JLT Capital Markets will target the corporate market to source weather ILS deals as a form of contingent business interruption (CBI) cover, after the closure of its recent Market Re private cat bond demonstrated investor demand for the risk.

-

The Caribbean catastrophe risk pool has made a payout of $261,073 to the Belize government following heavy rains earlier in the month.

-

Retro capacity dried up towards the end of the mid-year renewals, as incremental new demand created a challenge for buyers that entered the market late in the day.

-

The Fort Murray wildfire in Alberta has become the costliest natural disaster in Canada's history, with insured industry losses estimated to range from C$4.4bn and C$9.0bn ($3.4bn-$6.9bn), according to modelling firm AIR Worldwide

-

Modelling firm RMS has estimated that insured losses for the magnitude 7.0 earthquake that struck Japan's Kumamoto prefecture on 15 April will be between $800mn and $1.2bn

-

Reinsurer quota shares and the industry loss warranty (ILW) market are the most likely source of claims for ILS investors from the Fort McMurray wildfire

-

A wildfire in the Canadian city of Fort McMurray is likely to end up as one of the costliest natural disasters in the country's history, according to Aon Benfield's Impact Forecasting

-

The magnitude 7.8 earthquake which struck Ecuador on 16 April will produce total insured losses of between $325mn and $850mn, AIR Worldwide said yesterday (21 April).

-

Manufacturers including Toyota, Honda, Mitsubishi and Sony have closed factories in the Kumamoto prefecture after a 7.0 magnitude earthquake struck in the early hours of Saturday morning (16 April) local time.

-

Specific structures adapted to the ILS market are likely to be required if alternative capital is to expand more broadly into the corporate insurance sector, panellists at the Sifma IRLS 2016 conference agreed.

-

Aon establishes facility; Catco completed; UK flood losses £250mn-£325mn; Oppenheimer fund gains 4.93%; Blue Capital reduces net return target; Record hurricane season...

-

Cyber risk could create a bigger loss for insurers than a nuclear event, said AM Best, as it highlighted the potential for cyber losses to aggregate quickly from a single attack

-

AIR Worldwide estimated that the insured loss from the Chilean earthquake that occurred last week could be between $600mn-$900mn.

-

Fitch Ratings estimated that insured losses from the magnitude 8.3 earthquake that struck off the coast of Chile on 16 September were unlikely to top $500mn, with the bulk of losses being assumed by international reinsurers.

-

JLT targets corporate ILS opportunities; HCC plans weather growth

-

Florida-based managing general agency (MGA) New Paradigm Underwriters has begun writing parametric hurricane (re)insurance on Allianz paper, Trading Risk can reveal.

-

The Guernsey Financial Services Commission (GFSC) said that 45 percent of the 85 new insurance entities licensed during 2014 were linked to insurance-linked securities business.

-

The primary US insurance market could open up greater potential volumes of business to the growing ILS sector but there are several challenges ahead for funds trying to access this market.

-

Damage to Bermuda as a result of Hurricane Gonzalo may cost insurers $200mn to $400mn, modelling firm AIR Worldwide estimated.

-

Modelling firm RMS has released a $250mn industry loss estimate for the earthquake that hit the South Napa region in California last month, significantly below earlier estimates of the potential insured loss

-

The ILS team at Credit Suisse Asset Management estimated that insured losses from Sunday's Napa earthquake would reach about $1.5bn, according to a regulatory announcement from London-listed ILS fund DCG Iris.

-

The Californian earthquake that struck near the Napa Valley wine-producing region on 24 August may cost (re)insurers between $500mn and $1bn, catastrophe modelling company Eqecat estimated.

-

The first parametric transaction completed on JLT Capital Markets' Market Re private cat bond platform has raised $30mn of cover against North American earthquake risk.

-

Insurers are facing claims of $1.5bn from the cold weather that struck the US in January, according to Aon Benfield.

-

American International Group (AIG) is seeking to add $100mn to its Tradewynd Re cat bond reinsurance with a new shorter-term issuance that covers the same risks transferred in its $125mn July deal, Trading Risk understands

-

Insured losses from flooding within Germany alone could reach almost EUR6bn, catastrophe modeller AIR Worldwide has estimated

-

RMS said that the Oklahoma tornado that hit Moore on 20 May will rank as one of the costliest tornado events in history and is likely to cause insured losses of $2bn-$3.5bn but it is unlikely to hit the reinsurance market.

-

PCS has kept its loss estimate for Hurricane Sandy stable at $18.75bn but it has left its file on the disaster open, going against its normal policy of closing off the survey process once it has produced two consecutive stable loss estimates for a disaster.

-

PCS said the $7.75bn hike to its second loss estimate for Superstorm Sandy was almost entirely based on new market data rather than extrapolated estimates

-

Hurricane Sandy's unique profile will test how well the PCS industry loss compilation service covers certain claim categories, as buyers of industry loss-based covers wait to see where the event will settle.

-

US insurer Travelers expects to take $650mn of post-tax net losses relating to Hurricane Sandy. The firm estimated its gross pre-tax loss before reinsurance recoveries at $1.135bn.

-

Significant uncertainty continues around the ultimate insured losses from Superstorm Sandy as new forecasts flow in from modellers and reinsurers.

-

Attempts to model losses from Superstorm Sandy has presented some unique challenges, but nevertheless the storm fits within the expected range of outcomes for a north-east hurricane, modelling firms say.

-

Hurricane Sandy will have little impact on catastrophe bond pricing for new deals based on current loss estimates, Willis Capital Markets & Advisory (WCMA) said in its third-quarter report on the ILS market.

-

RenaissanceRe's sidecar DaVinci Re reported a $74.2mn profit for the third quarter, up from $9mn for the same period a year ago, assisted by a significant improvement in investment results as well as lower catastrophe claims.

-

Listed retrocession provider Catco says its 2012 returns could be reduced by up to 10-15 percent net if insured industry losses from Hurricane Sandy reach the upper end of modellers' estimates of $15bn, according to a statement from the firm.

-

Leading ILS fund manager Credit Suisse believes that insured losses from Hurricane Sandy could reach $14bn-$18bn, according to a statement from the London-listed DCG Iris fund

-

Credit Suisse Asset Management no longer expects Hurricane Isaac to have any impact to the portfolio of the listed DCG Iris fund.

-

Credit Suisse Asset Management expects to take a 0.2 percent hit to the net asset value (NAV) of its Low Volatility Plus Iris fund as a result of Hurricane Isaac, according to a disclosure from the listed DCG Iris fund.

-

Energy risk specialist CatVest Petroleum Services has officially launched its EnergyRisk Model to model catastrophic losses from offshore and onshore oil and gas facilities as it targets the industry loss warranty (ILW) risk transfer business.

-

Private cat bond deals are likely to continue, but they do not always save costs for their issuers, broker Willis Capital Markets and Advisory said in a recent report on the ILS market

-

The rest of 2011 and early 2012 should be a busy period for the cat bond market as pent-up demand from earlier this year is released, broker Willis Capital Markets & Advisory predicted today in its third quarter report.

-

New Zealand earthquake losses may have prompted some traditional reinsurers to question the value of lower-paying international risk this year, but the ILS market still seems intent on adding more breadth.

-

Catastrophe modelling firm AIR Worldwide (AIR) released updates to its European wind and earthquake cat risk models this week, with both models having been expanded to include additional countries.

-

Speaking at a Munich Re ILS panel in Monte Carlo today, Fermat Capital founder John Seo predicted that issuance prices for US hurricane catastrophe bonds could rise 15-25 percent on a steady bond structure under the new hurricane model from RMS.

-

Collateralised reinsurance supply could be hamstrung if further loss events tie up capital this year, Aon Benfield Securities said in its first-quarter report on the ILS market.

-

Risk Management Solutions (RMS) has issued a preliminary value for users of its Paradex index, setting the initial index number for the 11 March Tohoku earthquake at 3.1tn yen.