-

Reinsurers could use retained earnings to target growth and buy more retro.

Reinsurers could use retained earnings to target growth and buy more retro. -

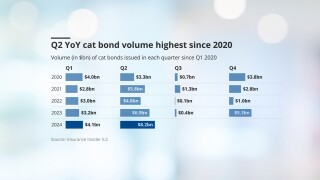

Cat bond market growth has exceeded broker-dealers' 2025 forecasts by some distance.

-

This was the second issuance completed by Farmers via its Bermuda reinsurance vehicle Topanga Re.

-

The Italian asset manager also plans to relaunch its multi-strategy ILS fund.

-

The finance committee discussed shifting market dynamics as tort reform takes effect.

-

CA Fairplan’s Golden Bear Re deal upsized 200% to $750mn.

-

PoleStar Re Ltd 2026-1 includes three sub-layers, which run for a three-year term.

-

The note is paying a spread of 975bps, 11.3% below the midpoint of the initial guidance range.

-

Man AHL Cat Bond Strategy has $1bn in assets, around 2% of Man AHL Partners’ total of $54bn.

-

The TPA approach to investing was adopted by US pension fund Calpers last month.

-

The total yield is down 162bps from 10.31% in the last week of November 2024.

-

Migdal Insurance placed its debut cat bond Turris Re for $100mn of quake limit.

-

The European ETF launch has benefited from the performance of the Brookmont US cat bond ETF.

-

The sponsor is offering two notes but will only place one depending on market interest.

-

Secondary market pricing implies the sponsor could recoup a total of $50mn on the 2022-1 A note.

-

One fund tracked by the index had a negative month.

-

The fund held $10mn in AuM, with $3mn the minimum investment required.

-

North Carolina Farm Bureau raised $500mn with its latest Blue Ridge Re cat bond deal.

-

Demand for top layer coverage may also need to be supported by underlying market growth.

-

The single note is offering an effective coupon of 23.5% at the midpoint of guidance.

-

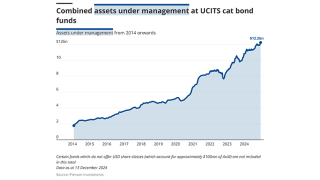

Assets under management in UCITS cat bond funds stood at $17.8bn as of 7 November, according to data from Plenum Investments.

-

The cat bond market is on course for $56bn of notional outstanding by the end of this year.

-

The two funds feed into the $892.5mn Schroder IF Flexible Cat Bond Fund.

-

The issuance will be the fourth deal offered by the Lloyd’s carrier.

-

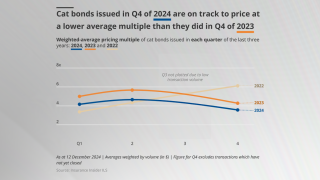

The shift in multiples is indicative of price softening in the cat bond the past two years.

-

The deal provides protection in Europe, after Mapfre Re’s debut bond last year covered US perils.

-

The average weighted spread on the deals was 651bps, skewed upward by cyber and wildfire deals.

-

The reinsurer is the second sponsor opting not to renew cyber coverage in the bond market this year.

-

The ratings agency first indicated it would consider a new methodology in March.

-

The single Class A note is offering an initial spread range of 1,050-1,150 to investors.

-

The sponsor has $140mn of cyber cat bond protection maturing in December.

-

One William Street priced its debut cat bond 13% below the midpoint of guidance.

-

The reinsurer-linked manager now offers three ILS funds encompassing private ILS and cat bonds.

-

The sponsor has $200mn of cat bond protection maturing in December this year.

-

Total yield is down from 11.18% in the last week of October 2024.

-

Covea’s Hexagon IV Re deal priced 13% below the initial target on a weighted average basis.

-

Total gains for the year reached 7.71%.

-

Some experienced investors are pivoting out of cat bonds and into the top layers of private ILS deals.

-

Central pressure of 900mb or below would trigger a full loss of the $150mn deal.

-

Pricing on Friday implied a potential $45mn loss to the bond, before the storm outlook deteriorated.

-

So far this year, there have been 11 first-time sponsors to place a deal.

-

Competition on price from traditional markets is weighing on bond market momentum.

-

The insurer of last resort’s exposure was $696bn as of last September.

-

The bond will provide protection against US wind with a PCS trigger.

-

The cedant’s current deal is due to mature at the end of January 2026.

-

Spreads on USAA’s latest deal priced below comparative issuances in 2023-2024.

-

Investor interest is warming up following a colder spell over the past several years.

-

The funds will combine credit and ILS holdings.

-

The hire is the hedge fund manager’s third ILS appointment in the past year.

-

Key topics include private ILS growth prospects and the longevity of longtail interest.

-

Returns from cat risk investments stood at 20.1% for the year to 30 June 2025.

-

The insurer of last resort currently has $2.15bn of cat bond protection on risk.

-

The alternative asset manager was founded in 2021 with offices in London, New York and Abu Dhabi.

-

Sources have said $1bn+ of fresh capital from the region is expected to be deployed in 2026.

-

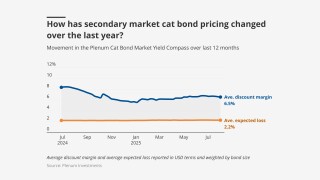

The figure comprises 5.48% of insurance discount margin and 3.96% of risk-free rate.

-

Pricing has hit historically soft market lows, based on secondary market pricing.

-

The manager’s largest ILS holding is in the cat-bond-heavy High Yield fund.

-

Cat bonds have outpaced the returns on private strategies in the year to date.

-

The new Verisk SCS model is increasing expected losses on aggregate bonds.

-

Deals would need to be sized at $50mn plus for transfer to capital markets.

-

The CEA had $19.3bn of claim-paying capacity as of 31 July.

-

The ILS manager has $6.8bn in assets and will be led by MariaGiovanna Guatteri.

-

The measures also seek to encourage greater wildfire mitigation efforts.

-

ILS executives talked pricing, capacity and opportunities in casualty at an ILS roundtable in Monte Carlo.

-

The market has learned lessons from earlier soft market phases that it will apply now.

-

Victory Pioneer Cat Bond Fund also added assets in the past month.

-

The figure comprises 6.07% of insurance discount margin and 4.15% of risk-free rate.

-

He added that Munich Re does not rely on retro or third-party.

-

The sponsor extended two notes issued in 2022.

-

The investment bank had stopped offering ILS services last September.

-

The agency noted inflows to cat bond funds and investor interest in private ILS.

-

Competition from cat bonds in the top layers of programmes applied downward pressure on reinsurance pricing in 2025.

-

Dedicated reinsurance capital is on track to increase by 8% in 2025, the broker said.

-

Funds encompassing private ILS outperformed cat bond strategies in July.

-

Market participants have until 13 October to provide any comments.

-

A trend towards higher-risk ILW bonds helped keep yields in double-digits despite softer rates.

-

The CUO has added the role of head of private ILS, joining the executive team.

-

ILS accounted for 2.5% of the pension fund’s total AuM.

-

ILS investors have fought shy of multi-peril aggs due to low confidence in SCS modelling.

-

The reinsurer’s chair said cat pricing reductions are at a “miniscule level”.

-

The yield figure comprises 6.53% of insurance discount margin and 4.28% risk-free.

-

The Texas insurer of last resort previously had to have funding for a 1-in-100 year storm.

-

The ILS Advisers Fund Index reported a profit of 1.11% in June.

-

Amid $17bn of new deals, cat bond activity included aggregate and cascading structures.

-

The bond will provide protection on an industry-loss basis, as reported by PCS.

-

The merged business of Twelve Securis ranked third among ILS managers for AuM, behind Fermat and RenRe.

-

Cat bond broking growth contributed to 6% organic growth in reinsurance.

-

The consultation period around UK ISPVs was opened in November last year.

-

Managers believed end-investors value diversification and non-correlation of cat bonds over liquidity.

-

Cat bonds remain attractive for investors seeking risk-adjusted return and diversification.

-

The PRA will also have to report on turnaround time for new approvals against 10-day and six-week targets.

-

The fund was renamed from the Pioneer Cat Bond Fund.

-

The total yield was 11.03% as of 27 June, including 4.3% of risk-free rate.

-

Some $400mn of bonds priced in the past week, after a record-setting H1.

-

The recommended “AIF lite” structure could be suited to cat bond lites.

-

This comes in at the lower end of the initial spread guidance of 725-775 bps.

-

The investment consultancy said yields increased in Q2 by less than could have been expected.

-

Property cat-focused sidecar capital was up by approximately 10% in H1.

-

The sidecars will provide capacity for reinsurers and large insurance carriers.

-

Initial responses to ESMA’s report welcomed the long timeframes for any changes.

-

Weighted average multiples were down as sponsors capitalised on demand to push spreads lower.

-

The total return for the Swiss Re Global Cat Bond Index stood at 0.61% for the month.

-

The body said cat bonds are closer to an insurance product than a security.

-

The awards celebration took place at the Hilton Bankside on 25 June.

-

Twelve Securis is now a challenger for the top spot on the Insurance Insider ILS leaderboard.

-

The bond is split across a Series 1 and Series 2 structure, with eight notes in total.

-

Everest Re increased the targeted size of Kilimanjaro Re across all four classes of notes.

-

M&A and shifts in distribution arrangements bring risks and opportunities.

-

Pricing on all classes of notes are being offered at the bottom of the guided range.

-

AuM in GAIA Cat Bond Fund had grown to $3.9bn as of 31 May.

-

PCS's loss estimate for the March Missouri SCS pushed the bond beyond its exhaustion point.

-

The California Earthquake Authority upsized its Ursa Re deal by 60% to $400mn.

-

The Californian insurer had a private deal, Randolph Re, that provided pure wildfire protection.

-

The firm said it was the first time a UCITS cat bond fund passed the $4.0bn mark.

-

Everest Re has structured its deal into two sections targeting aggregate and per occurrence cover.

-

The fund was set up 18 months ago by cat bond investor Florian Steiger.

-

Total yield was 10.93% as of 30 May, including 4.34% of risk-free rate.

-

This followed a $650mn fall in April, after management change of the fund.

-

A total $225mn of fresh limit entered the market across two deals.

-

The bond will provide protection for storms, quakes and fires in seven US states.

-

The bond protects against losses in the US, Canada, Europe and Australia.

-

The company also has $100mn for US hurricane events.

-

The index provider revised up its return for March by 0.39 percentage points to 1.21%.

-

The carrier previously raised a Finca Re cat bond in 2022.

-

The company is a wholly owned subsidiary of AmTrust Financial.

-

The carrier previously redeemed from a Herbie Re cat bond for California wildfire claims.

-

The deals covered Euro wind and Italy quake, Florida hurricane and a retro bond.

-

The ILS market has won market share at the top of programmes as buying expands.

-

The bond will provide protection for Allstate’s Florida subsidiary, Castle Key.

-

The Italian sponsor has $237mn of limit maturing this July.

-

The cat bond limit total is an uplift of around 60% on the carrier’s 2024 bonds.

-

Some assets in the Medici Fund were transferred to a new UCITS strategy.

-

The bond will provide named storm and quake coverage in the US.

-

The bond is offering a spread range of 850-925bps.

-

One dollar-denominated deal has opted to hold collateral in EBRC notes.

-

The bond will cover named storms in five US states.

-

Price guidance for the bond is 4.00%-4.50%.

-

The platform’s aim is to support the ILS industry in ‘getting the marks right’.

-

Debut sponsor SV SparkassenVersicherung also secured its target size of $100mn.

-

Proceeds will expand the company’s reinsurance protection in Florida and South Carolina.

-

Some $200mn of fresh limit entered the ILS market as $3.4bn of deals priced.

-

Sources believe the market will grow gradually over years after its initial cluster of dealmaking.

-

The bond provides coverage on personal-lines property in Florida.

-

The series one notes will provide protection to the benefit of Twia.

-

The total yield, inclusive of the risk-free rate, was down on the same period last year.

-

The bond will provide multi-peril coverage on an industry loss basis.

-

Gallagher Re said rates had softened in 2025 versus the prior two years.

-

The bond will provide storm protection in Florida and South Carolina.

-

Fermat and GAM announced that the former will take sole control of the GAM FCM Cat Bond Fund.

-

The deal will provide named Florida storm protection on an indemnity, per occurrence basis.

-

Florida Citizens upsized its latest Everglades Re deal by 50%.

-

The buzz in the air at ILS Connect told of a market entering its next growth phase.

-

The CEO said private ILS funds can generate additional returns of 10%-20%.

-

The state insurer of last resort is set to purchase $2.89bn of reinsurance this year.

-

Richard Pennay also addressed the dip in cyber ILS activity.

-

The renewal and upsizing of the Trouvaille E&S sidecar highlighted the market’s potential.

-

Private ILS would benefit from extension spreads to manage investor concerns, the CEO argued.

-

The bond will offer retrocession coverage for Hannover Re.

-

The catastrophe bond comes after the issuance of a Mayflower Re bond last year.

-

Its 2025 programme exhausts at $9.5bn excess $1bn.

-

All 29 funds tracked by the index returned a positive performance.

-

The bond will provide protection against named storm and thunderstorm.

-

Cat bond sponsors continue to secure higher limits and lower rates versus their targets.

-

Investor interest and capital flows point to potential for ILS proliferation.

-

The bond initially sought $425mn across three tranches.

-

The bond will cover China, India and Japan quake and Japan typhoon.

-

The bond will provide protection against German and Japan quake.

-

Secondary market traders are baking in further loss potential after PCS increased its wildfire and Helene loss estimates.

-

Franklin Templeton’s allocations to ILS are managed by fund of funds manager K2 Advisors.

-

The industry loss data provider also increased its estimate for Hurricane Helene to $15.3bn.

-

This is the first time the Texas Fair Plan has entered the cat bond market.

-

The deal of the size was unchanged at $100mn.

-

Portfolio rebalancing was not triggered last week, but investors are now distracted and nervous.

-

US Coastal Property and Utica Mutual Insurance have brought out their first cat bond deals.

-

The bond will provide protection against China, India and Japan quake, and Japan typhoon.

-

The subject business covers a portfolio of residential insurance.

-

The sponsor is estimating a loss of ~$300mn in relation to one of last month’s US tornado events.

-

Sutton National and Bamboo Ide8 secured $170mn of sidecar and cat bond protection.

-

The bond will provide coverage against named storm or severe thunderstorm over three years.

-

Torrey Pines Re is split among three tranches of notes.

-

The issuance is split across three tranches with varying degrees of risk.

-

The deal is split across four tranches, with the riskiest note Class D targeting $150mn.

-

The cat bond will initially cover named storms in Florida and South Carolina.

-

Market participants expect pricing will be flat to down through Q2.

-

The bond will provide protection against Louisiana named storm.

-

Fees on the GAM Star cat bond funds will drop in May in a recognition of fee competition in the market.

-

The sponsor secured $240mn of limit as the bond upsized by 20% on its initial target.

-

The insurance discount margin is now at a similar level to where it was in the final week of March 2022.

-

Most of the ILS investments were made via the cat bond heavy High Yield Fund.

-

Palm Re will provide Florida named storm cat bond coverage for Florida Peninsula, Edison and Ovation Home Insurance Exchange.

-

Multiples in March were below historic averages from 2001 through 2024.

-

The ETF will invest solely in natural catastrophe-exposed bonds.

-

Scor is targeting limit of $200mn with its latest Atlas DAC retro cat bond.

-

The notes replace a 2021 issuance that matured in January this year.

-

The deal is 45% larger than 2024’s issuance after attracting a “greater number of investors”.

-

The cedant’s Namaka Re bond is offering a spread range of 200-250 bps.

-

The bond provides coverage for North American storms and earthquakes, as well as European windstorms.

-

The pricing is at the top end of the initial guidance range of 550-600bps.

-

The bond is being issued through Lloyd’s London Bridge 2 platform.

-

The bond upsized by around 20% as pricing settled 2% below initial guidance at 7%.

-

The bond will provide coverage for Japan typhoon and flood on an indemnity, per-occurrence basis.

-

Caution about capital markets volatility is leading sponsors to stagger bond renewals.

-

The ILS segment is not ready to gloss over loss-heavy years in renewal discussions.

-

The mega cat bond season in Q2 last year recorded issuance of $8.2bn.

-

The agency said introduction of a new methodology will depend on the feedback it receives from the ILS market.

-

Guernsey’s TISE listed the world’s first private cat bond issued by Solidum Re in 2011.

-

Founding partners DeCaro and Rettino will continue to provide oversight and investment advice.

-

This will be the third cat bond issuance through Baltic Re PCC.

-

The cat bond manager warned of excess downside risk owing to an accumulation of losses.

-

Flood Re’s bond Vision 2039 bucked the trend by pricing up 7% as its secured £140mn ($174mn) of limit.

-

Island appetite remains stable, but early 2025 loss activity has injected fresh uncertainty.

-

The reinsurer had taken the opportunity to buy more limit across event and aggregate covers.

-

The bond was trading at around 12.3c on the dollar in the secondary market last month.

-

This year’s coverage will involve $2.94bn of new risk transfer.

-

This will be Brit’s first cat bond issuance since its 2020 deal through Sussex Capital.

-

The deal is being issued through Lloyd’s London Bridge 2 PCC.

-

Some $4.8bn of reinsurance and cat bond limit will come up for renewal in 2025.

-

Some $625mn of new issuance entered the market in the first week of March.

-

There is the potential for cat bond H1 issuance to be a record breaking six months.

-

The scope of QRT’s new ILS strategy will include cat bonds and private ILS.

-

As of 14 February, the company received 405 claims.

-

The fund is open to European and other global investors.

-

The bond will provide fire protection for MGA Bamboo’s California business.

-

Dispersion of returns was high, with the range 0.87% to -3.71%.

-

The coverage will be on an indemnity, per-occurrence basis.

-

The bond will cover named storms in the state of Florida.

-

The cost of reinstatement was included in $170mn wildfire net loss figure.

-

Deal sizes increased by 84% on average across the six tranches that saw an increase.

-

The Class A section of the bond has doubled in size, at lower pricing.

-

The firm has rotated capital in sidecar Voussoir toward direct investor relationships.

-

The NCIUA had initially sought $350mn of limit.

-

The state-backed carrier has $2.1bn of Alamo Re cat bond coverage.

-

UCITS fund diversification targets limit their capacity for US wind bonds.

-

Pricing fell by 13.5% on a weighted average basis across deals that updated last week.

-

Several Florida start-ups are poised to begin writing business this year.

-

Modest increases to reinsurance costs were partly offset by the Australia cyclone pool.

-

The estimate is net of its per-occurrence reinsurance program and gross of tax.

-

The aim is to capitalise on cat bond market’s robust growth and US peril concentration.

-

The loss aggregator has classified the fires as two separate events for reinsurance purposes.

-

New limit of $474mn entered the market across two deals.

-

The Class B segment of the bond has priced below initial guidance.

-

Wildfire is rarely singled out as an exposure that can shift portfolio outcomes.

-

The bond provides coverage for storms, earthquakes and severe weather events.

-

Two ILS funds featured in the top five asset-raisers within the index.

-

The fall marks this the first time in 20 years the index has been negative in January.

-

The firm will match segregated accounts of portfolios to investor mandates.

-

The deal is being issued through Lloyd’s London Bridge 2 PCC.

-

The combined entity ranks third in the Insurance Insider ILS leaderboard.

-

Liquid alternative strategies accounted for around $1.4bn of the total.

-

The bond is likely replacing the 2021-1 Class F bond, which matured in December.

-

AuM remains generally flat at UCITS funds over the weeks since LA fires started.

-

The bond will provide coverage for named storms in North Carolina.

-

American Integrity is seeking expanded limit on more favourable terms.

-

But cat bonds are experiencing negative secondary market price movement.

-

Tower Hill secured $400mn of Winston Re limit in 2024.

-

The sponsor secured $100mn limit last year, paying a multiple of 8.3x.

-

The carrier has recognised two separate losses for the Palisades and Eaton fires.

-

Capital inflows, notably into UCITS funds, and accumulated returns supported issuance of $17.2bn in 2024.

-

The deal priced below guidance for the Class A and Class B tranches.

-

The carrier previously raised $125mn via an Ocelot Re cat bond in 2023.

-

The Integrity Re bond is structured into five tranches.

-

The deal has upsized by around 64% compared with the initial target.

-

The offering is a collaboration with Generali and parametric carrier Descartes.

-

The reinsurer added two new tranches to its 2025 issuance.

-

Peril- and geography-specific deals are being well received by investors.

-

A negative January return will be unprecedented for ILS industry.

-

The index delivered a total return of 1.29% for the month of December.

-

The bond went on watch after Mercury said it would exceed its $150mn retention.

-

Company touts growing investor demand for Asian cat risks.

-

Both the Class A and Class B notes increased in size.

-

The latest issuance will add extra cat bond limit, with a $100mn note still on risk.

-

-

Secondary pricing on the carrier’s Topanga Re bond partly recovered following the guidance.

-

Fermat stayed in the top spot surpassing $10.0bn for the first time.

-

Secondary market pricing indicated anticipated California wildfire losses.

-

The reinsurer has issued updated pricing for the instrument.

-

Theo Norris joins from Gallagher Re, which brokered one of the first 144A cyber cat bonds.

-

Two 2021 worldwide aggregate ILW notes are also among the markdowns.

-

The bond is split into five tranches, with two notes offered on a zero-coupon basis.

-

Price guidance for the bond is 7.00%-7.75%.

-

The vehicle has $2.55bn in capital committed by institutional investors.

-

The bond is likely replacing the 2021-1 Class F bond, which matured in December.

-

The fund returned 15.69% in calendar year 2024.

-

This comes after the firm’s distribution partner GAM has had a challenging few years.

-

ILS managers expect the losses to have some impact on future cat bond spreads.

-

The reinsurance attaches at $7bn, unchanged for the past two years.

-

Aetna, Inigo and GeoVera were the three sponsors seeking lower multiples.

-

The index’s performance in November was stronger than the prior year, although YTD returns are behind 2023.

-

Compressed cat bond spreads could drive some rebalancing, as M&A remains a prospect.

-

Plenum said impact is marginal because wildfire contributes only marginally to the risk of bonds.

-

The ILS manager analysed 16 UCITS fund portfolios to compare risk levels.

-

The reinsurer is seeking annual aggregate cover against earthquakes and second-event named storms.

-

The sponsor has expanded its target deal size compared with a year ago.

-

The first cat bond deal from the carrier achieved its target size of C$150mn.

-

The reinsurer is seeking index-based cover for a wide scope of perils and territories.

-

The deal is split into two tranches compared with the single note issued last year.

-

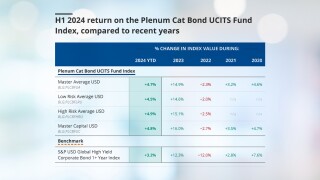

Cat bond investors have earned a cumulative 39.6% over 2023 and 2024.

-

Novelty premiums will likely fade once investors are more comfortable with the risk.

-

Spread guidance anticipates a lower multiple compared to 2024’s Vitality Re issuance.

-

The forecasts anticipate a large volume of maturities and rising sponsor demand.

-

The manager’s Interval Fund returned 28.25% over the financial year.

-

Cat bonds were a key supply-side driver at 1 January 2025.

-

Investment in the space comes mainly from the cat bond market, Gallagher Re said.

-

The broker anticipates strengthening investor demand for collateralised re.

-

Over-subscriptions have been evident on well-priced US cat treaties.

-

The Bermuda based entity is expected to continue on its “responsible growth trajectory”.

-

First-time sponsor QBE secured $250mn of quake and storm coverage.

-

The UCITS cat bond segment has added 54% in AuM since Hurricane Ian.

-

Some $1.2bn of limit was placed in the cat bond market this week.

-

The $600mn fund could allocate up to 10% of assets to cat bonds from 2025.

-

Initial spread guidance for the three-year bond is set at 425-500bps.

-

The firm will also act as sub-adviser to the Brookmont ETF cat bond fund.

-

Recoletos Re DAC SPI takes its name from the Paseo de Recoletos boulevard in Madrid.

-

The carrier has raised $75mn of higher-risk Class C coverage.

-

The bond offers a higher multiple than a similar Fuchsia Re deal placed last year.

-

The bodies said that tapping into the cat bond markets was a possibility.

-

The Class A and C notes increased in size, while the Class B note remained unchanged.

-

MMIFS Re is the debut cat bond offering from the Canadian carrier.

-

Mapfre Re CEO Miguel Rosa was “very satisfied” with the debut cat bond deal.

-

Overall, reinsurers accepted that rate cuts were still leaving them with strong margins.

-

Full year 2023 set the record to beat of $15.8bn in new issuance volume.

-

The bond will provide multi-peril coverage in the US and District of Columbia.

-

The former co-head of ILS at Schroders left the bank last month.

-

The pricing multiple on the deal is 12.1x the sensitivity case expected loss.

-

The single Class A note is paying a multiple of 2.1x.

-

The Class A and Class B notes are paying lower multiples than initially guided.

-

Beazley returned with its second Fuchsia cat bond issuance.

-

The bond will provide coverage for named storm across five US states.

-

Former ILS investors who left the space have looked again and re-allocated.

-

The ILS manager’s existing Medici cat bond strategy stood at $1.68bn in assets under management (AuM) as of 30 September.

-

Pricing on the Class A and Class B notes settled below guidance.

-

The bond will provide named storm and quake coverage.

-

The 2025 target would be ~25% larger than the $3.56bn it placed for 2024.

-

The $100mn note was unchanged in size.

-

Fidelis is seeking more cat bond cover than it did almost a year ago.

-

Losses from Hurricane Milton are expected to affect only select junior structures.

-

The fund will invest in listed and private transactions.

-

The Class B notes on the carrier’s debut deal attach at $500mn of losses.

-

The bond will provide aggregate coverage against named US storm.

-

The bond is split into three tranches of notes.

-

This is the second time Fidelis has entered the cat bond market this year.

-

The latest clutch of offerings indicates pricing discipline in the bond market.

-

Moderate impacts to ILS returns are anticipated from Hurricane Milton.

-

Athena Re provides coverage against terrorism in France and its overseas territories.

-

The deal is offering a multiple of 13.6x on the sensitivity case expected loss.

-

The association’s Hurricane Beryl net loss stood at $455mn as of 30 September.

-

The UCITS fund was launched in 2021 and invests in cat bonds and the money markets.

-

The headline figure of $7.72bn includes $3.11bn of DaVinci equity plus debt.

-

The bond is targeting $225mn of limit across the Class A and Class B notes.

-

Spreads at levels favourable to sponsors could power Q1 2025 pipeline.

-

The consultation period closes on 14 February 2025.

-

The notes provide coverage in the US and District of Columbia but exclude Florida.

-

The latest issuance is the second cat bond RenaissanceRe has issued this year.

-

Fema's traditional reinsurance programme will attach at losses of $7bn and above.

-

Cheaper traditional reinsurance as of mid-year may have dampened deal pipeline.

-

The failure of a Jamaica bond to pay out following Hurricane Beryl damage has brought focus onto the deals.

-

In other property, Helene and Milton will assure rates remain attractive, he added.

-

The latest issuance signals the second time the sponsor has entered the cat bond market.

-

The bond offers a midpoint multiple of 4.1x with an expected loss of 0.92%.

-

The firm’s AuM in four key vehicles rose $526mn in Q3.

-

CEO Adrian Cox said Beazley’s recent $290mn ILW purchase was not driven by “capital flexibility in and of itself”.

-

Michael Rich left the portfolio management role in May.

-

Latest pricing suggests secondary market traders are baking in further loss development.

-

The bond provides protection in France and its overseas territories.

-

September was the strongest performing month since the index began in 2006.

-

Some $409mn of volume entered the market in the week to 4 November.

-

The low PCS number is presenting a challenge for ILW buyers and sellers.

-

The figures imply first-layer reinsurance recoveries for Helene.

-

The four-year deal is split across three tranches of notes.

-

The latest issuance offers a spread range of 650-700bps.

-

The final price fell 14% from the initial midpoint price offered by the sponsor.

-

The NFIP’s traditional reinsurance coverage kicks in at $7bn of losses.

-

The deal would represent a diversifying auto risk deal.

-

Pricing is expected to “stay neutral of soften” for January renewals.

-

The sovereign wealth fund’s ILS investments grew to $828mn.

-

Cat bonds, private ILS and retro were all kept at “strongly overweight”.

-

Managers expect Hurricane Milton losses to shore up pricing.

-

Many in the ILS sector are bullish on Milton losses falling at the lower end of earnings impacts.

-

Losses from the hurricane may not significantly impact on many funds’ annual returns.

-

Florida domestics, aggregate retro and flood deals were all marked down.

-

The multiple offered on the deal is around 2.5x the expected loss.

-

The bond triggers on a parametric, per occurrence basis, across Class A and Class B tranches.

-

Icosa said certain cat bonds could see more than 0.2 points of price movement.

-

Plenum said wind damage from Milton could lead to “moderate” losses for its cat-bond funds.

-

Hurricane Milton will show the ILS product behaving as investors expect it to.

-

The company is monitoring the NFIP’s flood-exposed bonds.

-

This is a far narrower drop than post Ian, when the index was lost 10%.

-

A client presentation from the broker put total insured losses at $25bn-$40bn, leaving the Citizens and the National Flood Insurance Programs clear of reinsurance impacts.

-

Losses to the NFIP-sponsored cat bonds remains a key area of uncertainty, the investment manager reported.

-

The hurricane is likely to prevent rate reductions in property cat in 2025.

-

This is based on insured loss estimates of between $20bn and $60bn.

-

Integrity Re 2024-D and Lightning Re 2023-1A are two bonds that were marked down, although no trading has occurred.

-

Hurricane Milton’s overall impact, based on the current pre-landfall scenario, could lead to “moderate losses” for Plenum’s funds.

-

Collateralised reinsurance and retro are in the firing line.

-

The government-backed scheme has greater take-up in areas in Milton’s path.

-

The Mexican cat bond offers $125mn of protection against Atlantic named storms.

-

Most sources noted expectations of a $50bn+ event, but the range of outcomes is huge.

-

Parts of the Yucatan peninsula are under a hurricane warning, though the storm is expected to remain offshore.

-

The class of 2023-24 cat bond funds will grow existing investors and add new ones.

-

Richard Pennay will become CEO of Aon Securities.

-

The deal has reduced the carrier’s one-in-250-year cyber loss scenario from $651mn to $461mn.

-

The strategy invests in subordinated bonds issued by European insurers.

-

The storm made landfall as a major hurricane in Florida’s Big Bend region.

-

Only three storms have impacted a larger area than Helene since 1998.

-

The cat bond application process will be streamlined to 10 working days.

-

The ILS manager expects “minimal, if any, losses” to bonds in its funds.

-

Maya Henry will be tasked with raising capital and managing clients in North America.

-

The ETF format provides for publication of a daily NAV.

-

The deal is offering a multiple of 11.3x on the expected loss.

-

The broker replaces Goldman Sachs on the business after the bank ceased offering ILS services.

-

The bond offers a multiple of 11.3x based on a modelled expected loss of 0.93%.

-

Brokers expect strong competition at remote risk layers at the 1 January renewal.

-

A strong forward pipeline will require fast work by ILS investment houses.

-

The sponsor has kept $25mn of principal in extension for any further loss development.

-

The ILS industry offered 11 points of merit that justify cat bonds being eligible for UCITS funds.

-

Kin’s reinsurance structuring means the bond’s losses will be kept to a minimum.

-

Most of the ILS capital was attracted to the cat bond market.

-

Demand for peak peril retro increased significantly in Q2 2024.

-

Cat bond funds continue to draw interest as private ILS more challenged.

-

The headline figure of $7.15bn includes $2.91bn of DaVinci equity plus debt.

-

The number of sponsors has risen from 46 about a year ago to 66 over the last 12 months.

-

The broker said it expects strong ILS capital inflows to continue.

-

The bond is offering a spread range of 950-1,050 basis points.

-

-

The US carrier abandoned the project due to high price expectations.

-

The Bermuda regulator is consulting on a refresh of its rules that will be in force as of 1 January 2025.

-

Growth was driven by strong returns and new investors entering the market.

-

Building better exposure datasets could draw a broader range of investors.

-

The insurer currently has $300mn of reinsurance limit from cyber cat bonds.

-

-

Quick-moving cat risk trading may become more prevalent in the ILS market.

-

The timing is “opportune” to start the strategy according to Bennelong.

-

Returns were down on 2023, which benefited from favourable Ian loss development.

-

The firm predicts 2024 will be a record year for primary issuance.

-

Florian Steiger’s strategy is seeking institutional capital for the Q4 primary issuance season.

-

The firms’ partnership preceded Japan's first ‘megaquake’ warning.

-

Several bonds suffered declines in value from February to July.

-

The deal takes year-to-date cat bond lite issuance to $367.6mn

-

The carrier estimates the total industry loss for the Microsoft/CrowdStrike outage at around $1bn-$2bn.

-

The board of directors has voted for a 10% rate hike.

-

The moves mark a major step in realising “trillion dollar” casualty ILS potential, according to Ledger Investing CEO Samir Shah.

-

-

The broker is yet to participate in a cyber cat bond.

-

The manager is looking to buy positions on the secondary market.

-

The rise is equal to 5%-10% of catastrophe capacity purchased, including cat bonds, depending on region.

-

Two Eclipse Re notes totaling $34.8mn were issued last week.

-

Cat bonds, private ILS and retro are "strongly overweight".

-

The property market remains “one of the most favorable ... I've seen in my career,” the executive said.

-

The market is expected to seek additional exclusions around systemic events.

-

Hannover Re's cyber bond pays on a parametric basis for each hour after an agreed waiting period.

-

The analyst estimated Beazley’s loss from the global outage at $80mn-$120mn.

-

Aeolus increased its participation on the program more than fourfold.

-

In 2023, Berkshire provided around $1bn in capacity to the Floridian insurer.

-

The carrier purchased an additional $150mn of cover.

-

The event could unpack issues around accumulation risk and cloud services.

-

The EUR150mn bond provides windstorm coverage in France and Monaco.

-

More than 30% of the fund's AuM is allocated to US windstorm-linked bonds.

-

Twia’s analysis showed existing rates were inadequate.

-

The firm has observed a “more widespread investor base” in cat bonds.

-

The fund follows an earlier climate change-focused ILS initiative from the firm.

-

Industry losses of $800mn-$1.2bn are expected from Beryl's impact in Texas.

-

The $1.6bn of cat bond limit on-risk includes $1.1bn Everglades Re mega-bond.

-

Secondary market activity and hedging would be likely if a Beryl-sized storm tracked toward the US.

-

This is lower compared to 8.2% recorded by the index in H1 2023.

-

The latest Insider ILS Outstanding Contributor for the year said 2011 was an under-appreciated turning point for the market.

-

The parametric trigger on the World Bank deal specifies storm pressure of 955mb or lower but its initial reported landfall was at 975mb.

-

Hurricane Beryl is expected to strengthen again after hitting the Yucatan Peninsula.

-

The parametric structure would have paid out at slightly lower storm pressure.

-

-

Benefits of ILS smart contracts include transparency and tradeability.

-

Recent modelling predicts a strong probability of direct landfall in Jamaica.

-

The manager’s ILS allocation has grown by 16% since 31 October 2023.

-

-

The latest Kilimanjaro Re, 3264 Re and Gateway Re deals all priced.

-

Cat bond spreads stabilised as maturities brought capital to deploy into the market, after an earlier spike.

-

Grenada and St Vincent and the Grenadines are under the most threat from the storm.

-

The broker estimated ILS capacity reached a record $107bn as cat bond interest surged.

-

The broker said high ILS maturities would boost cat bond issuance though the hurricane season would impact capital availability.

-

The broker said it did not anticipate a slew of new entrants, with the possible exception of casualty start-ups.

-

DeCaro is one of the cohort of pioneering ILS managers.

-

The broker said the mid-year reinsurance renewals benefitted from “more than ample” capacity.

-

The bond will provide named storm coverage on a county-weighted industry-loss basis.

-

The bond’s pricing for southern US storms landed at the upper bound of guidance.

-

The bond is offering investors a midpoint multiple of 5.5x.

-

The bond is seeking coverage for any named storm or earthquake event.

-

Cat bond deals placed last week amounted to $150mn of issuance.

-

The bond is seeking coverage for named storm, severe thunderstorm and winter storm.

-

The proposal now goes to the Florida Office of Insurance Regulation for review.

-

The deal was offering spread guidance of 525-600 bps with a mid-point multiple of 7.8x.

-

The deal is offering a multiplier of 6.6x on the expected loss.

-

A degree of pricing volatility was evident in the market this week.

-

The bond has priced at the mid-point of guidance.

-

The cat bond will provide coverage across multiple territories in Europe.

-

Pricing on the Class A notes settled 11% below guidance.

-

The reinsurer narrowed the scope of perils in its latest issuance versus its 3264 2022 cat bond.

-

Former Teneo M&A head Alexander Schnieders will lead the unit.

-

The shift in market dynamics reflects $1.8bn of maturities last week.

-

The bond is split across Class A and Class B notes that have different levels of risk.

-

Totara Re, placed last year, provides part of the reinsurance protection.

-

The cat bond market was very active in April as spreads began to widen.

-

The Icosa Cat Bond Strategy now stands at $130mn in AuM.

-

Tanja Wrosch joins Twelve after more than a decade at Credit Suisse ILS.

-

Market sources are speculating on the reasons behind the spread widening on index-based deals.

-

Additional capacity for upper-layer coverage is driving rate reductions, the broker says.

-

The bond is offering investors a spread range of 1,050-1,150 bps.

-

The carrier is returning to the cat bond market for the first time since 2020.

-

Rich had spent 13 years at the firm where he began his career and oversaw a cat bond and ILS portfolio.

-

The Swiss Re veteran left her former employer last year.

-

The company increased its full year 2024 adjusted net income guidance.

-

Concerning hurricane forecasts are among the factors driving tighter reinsurer capacity.

-

Torrey Pines, Atlas Capital and Marlon priced and sized up.

-

The fund has been badged with the Fermat name.

-

The Class A notes are offering pricing in the range 850-950 basis points.

-

Top layer competition is an added pressure on ILS firms, but the impact can be overstated.

-

The bond provides named US storm coverage and US and Canada quake protection.

-

-

The hires represent a reunion of colleagues from Horseshoe/ Artex.

-

The proposals include increasing either statutory or CRTF funds.

-

The program includes all perils coverage and third-event protection.

-

The four-year deal will be the second Nature Coast Re bond issuance.

-

The multiple on the Class A notes is lower compared with last year.

-

Florida Citizens' Everglades Re bond priced up by 6% across three tranches.

-

CEO Wagstaff said the LMG must "compete with other markets".

-

The second part of the PoleStar Re issuance takes the bond's total volume to $300mn.

-

Minors has experience working on insurance and reinsurance matters

-

Citizens also secured $1.1bn of limit for its Everglades Re cat bond.

-

Spreads on all tranches of notes settled above the initially guided range.

-

The capital will be allocated to a pure cat bond strategy, sources have confirmed.

-

The former Neuberger Berman managing director confirmed the new role in a LinkedIn post.

-

Longleaf Pine Re priced, while spreads on Everglades Re deal moved higher.

-

Spreads could continue widening throughout the rest of the year.

-

Cession ratios declined at three of the four publicly listed Floridians.

-

The company plans to reduce its quota share to 20% from 40%.

-

The sponsor was targeting between $850mn-$1.1bn of coverage in the latest mega-bond to hit the ILS market.

-

Rates are still materially higher than pre-pandemic and lower layers are holding firmer.

-

Twia needed to purchase $3.35bn of reinsurance to satisfy its $6.5bn 1-in-100 PML.

-

The index-based coverage will be for the benefit of Lloyd’s Syndicate 1910.

-

Combined AuM of UCITS funds stood at $11.3bn as of 26 April 2024.

-

The Mexican government’s IBRD quake bond priced 4% ahead of guidance.

-

The flat growth is a result of multiple forces influencing capital flows in both directions.

-

The new Marlon bond offers multiples of 7.4x and 8.9x on the Class A and Class B notes respectively.

-

Sanders Re cat bond coverage attaches higher than last year at $5.46bn.

-

The Class D notes offer a spread of 1200bps with a multiple of 2.9x.

-

California is the initial covered area but, following a reset, all US states will be covered.

-

The coverage will be annual aggregate with an index trigger for wind and quake.

-

First event tower for the Northeast exhausts at $1.1bn, at $1.3bn for Southeast and $750mn in Hawaii.

-

The pricing fell 13.7% on the Class A notes and 6.5% on the Class B notes.

-

Diversification in perils and regions can help the market grow.

-

The parametric bond provides coverage for named storms.

-

Its Class 13 and 14 notes priced roughly at the midpoint of expectations.

-

The World Bank’s Michael Bennett was speaking at the Insurance Insider ILS conference.

-

The deal will expand the region and perils covered by Merna Re bonds.

-

The fund has a strong focus on cedant quality and transaction structures.

-

Pricing increased by 28% on the Class A notes and 22% on the Class B notes.

-

The carrier has previously tapped capital markets with Cape Lookout Re transactions.

-

The carrier currently has $1.15bn of Merna Re cat bond limit on risk.

-

The coverage will be indemnity, annual aggregate for Florida named storm.

-

The Class A notes priced well below the midpoint of initial guidance.

-

The final pricing has settled toward the midpoint of the initially guided range of 225-250bps.

-

Aspen said reduced reinsurance appetite made it a good time to seek alternative capacity.

-

The new global bond fund can take a ‘marginal allocation’ to cat bonds.

-

The carrier’s Armor Re deal upsized by 33%.

-

The bond will cover named storms, North American earthquakes and European windstorms.

-

The World Bank-backed deal is structured with a parametric trigger.

-

The reinsurer said it hopes to grow the size of the $13.75mn deal over time.

-

-

The carrier of last resort is proposing total risk transfer of $5.5bn.

-

Retained earnings resulting from reduced loss activity also helped to boost ILS capital.

-

The coverage will be for named storm and quake.

-

The former Ledger director was joined by fellow ex-Ledger employees to “hit the ground running”.

-

The sponsor’s debut cat bond upsized by 25%.

-

The bond is the second transaction from the sponsor to target per occurrence coverage.

-

The bond will cover named storms in the state of Florida.

-

The mega bond has upsized to more than twice its initial target.

-

The coverage will be parametric based on the central pressure of the storm.

-

The final pricing is as the top end of the recently updated estimate.

-

Initially, the government sought $360mn of coverage.

-

ILS returns in 2023 sparked a flurry of enquiries from hedge funds.

-

-

This is up from the recent increase to $1.2bn.

-

The cover will be triggered on an indemnity, annual aggregate basis.

-

This came as the broker earmarked “material softening” of minimum traditional rates on line.

-

Proceeds from the sale will be used to fund sustainable development projects.

-

The carrier’s mega bond is seeking coverage for Texas named storm.

-

The carriers are seeking $130mn of Class C named storm coverage.

-

-

The carrier has updated the pricing guidance to 8.75%-9%.

-

The bond will cover named storms in the state of Florida.

-

Drop-in capital has now largely left the cat bond market.

-

The multi-peril coverage was due to expire in June 2026.

-

The platform distributed ~$50mn to investors for 2023.

-

The carriers are seeking $130mn of Class C named storm coverage.

-

The bond is Allied Trust’s debut issuance.

-

The cedant’s Namaka Re bond is offering a spread range of 225-250bps.

-

The two classes of notes are sponsored by separate insurers.

-

The carrier has priced the Class A tranche at 525 bps.

-

Chris Parry said the denominator effect remains a suppressant on ILS inflows after a strong phase of returns.

-

The carrier also narrowed the pricing guidance for the two types of notes.

-

-

A diverse investor base is among market characteristics seen as important for growth.

-

Proceeds from the bond will be used to fund IBRD projects.

-

The carrier has priced the Class A tranche at 500 bps.

-

Pricing on the Class A notes is at the lower edge of guidance.

-

The pricing guidance is now 550-575 basis points.

-

This year, the association’s funding will come to $4.05bn with a $2.45bn retention.

-

The RfP covers the CEA and/or the California Wildfire Fund.

-

The carrier has added $5mn to the target limit bringing it to $105mn.

-

Managers are hoping strong returns in 2023 will aid capital raising efforts.

-

Pockets of new capital will not shift pricing at mid-year.

-

Pricing on the Class A notes moved toward the lower edge of guidance.

-

The state carrier is moving to redeem its 2022 Everglades issuance a year early.

-

-

-

The carrier is seeking to raise $100mn of coverage.

-

The carrier is seeking named storm coverage in the state of Texas.

-

The carriers are seeking up to $130mn of named storm coverage.

-

The coverage is for any named-storm loss event in Florida.

-

The state pool is seeking indemnity, annual aggregate cover.

-

Sources are expecting multi-billion new limit to be placed.

-

The bond will provide named storm coverage in southern US states.

-

The bond will provide named storm coverage in some US states.

-

The bond will provide parametric cover for earthquake and windstorms.

-

The cat bond now has a pricing spread of 250-275 bps.

-

The cat bond will initially cover named storms in Florida and South Carolina.

-

The cat bond will cover earthquake and named storm events.

-

Some $415mn of capacity entered the market last year.

-

Pricing guidance has also been updated to between 8%-8.25%.

-

Estimates were revised from $845mn to $740mn.

-

The bond will provide protection against Japanese flood and quake events.

-

Sabine Re marks Allied Trust’s entry to the market.

-

ILS platform London Bridge II has had a good year as volumes reached $750mn, the CFO said.

-

-

The bond will provide named storm coverage in southern US states.

-

All funds tracked returned a positive performance.

-

Exposure updates played a greater role than expected.

-

The bond offers earthquake cover for several European countries.

-

The cover will include the 50 US states, District of Columbia and Canada.

-

The bond is structured into four tranches of notes.

-

-

Class A notes are priced at 1,400bps, Class B at 1,725bps.

-

Sources said preparations for a 2024 IPO were halted, but work could resume later this year.

-

Pricing and sizing details were provided for the Class C notes.

-

The spread guidance on both notes has moved lower.

-

The bond will insure against named storms in eight US states.

-

The vast majority of 2023 recoveries were from events in prior years.

-

The notes were further marked down after a year-end Ian loss update.

-

The state pool is seeking indemnity, annual aggregate cover.

-

The bond provides three-year aggregate earthquake coverage in Japan.

-

The cover will include the 50 US states, District of Columbia and Canada.

-

The rise was helped by performance fees at DaVinci.

-

Twia’s actuarial and underwriting committee made the recommendation last week.

-

The expected spend is around 33% higher than Twia had budgeted.

-

Sponsors still secured terms that were favourable relative to traditional cover.

-

Pricing for both falls at the lower end of the recently updated estimates.

-

Pricing settled toward the lower end of guidance.

-

Monthly cat losses were driven by two major events.

-

The bond is trading at 70c-75c in the dollar in the secondary market.

-

The carrier is targeting annual aggregate cover with a PCS index trigger.

-

The increase in limit reflects the carrier’s growing exposure.

-

The issuer is seeking aggregate and per occurrence coverage.

-

The pricing guidance on the Class A notes has moved to 1,025-1,075 basis points.

-

The bond is seeking per occurrence, state-weighted industry loss-based coverage.

-

Aside from the one-year view, 2023 remixes the track record.

-

The manager’s conservative strategy posted returns of 7.61%.

-

The carrier is now offering up to $250mn of Class A notes and $150mn of Class B.

-

The guide pricing offers similar multiples to last year’s issuance.

-

The claw-back is anticipated after PCS revised down its Ian loss estimate.

-

The index posted a positive return in each of the 12 months of last year.

-

The client lacked options in the conventional insurance market.

-

-

The bond is currently trading at around 65c in the dollar on the secondary market.

-

The Bermudian said its third-party vehicles were “sufficiently capitalised”.

-

Fourth quarter inflows also included $111mn for its retro platform Upsilon

-

The deal is a large expansion on last year’s cat-bond coverage.

-

The Medici cat bond fund experienced the largest growth in AuM.

-

The $175mn bond is priced lower than the original range set out in January.

-

The depth of the retro market recovery will be an influential factor in the pace of the cat market slowdown from here.

-

The firm told investors yields in the cat bond market are 'still very attractive'.

-

The transformer vehicle issued $209mn worth of cat bond lites in 2023.

-

Pricing is now targeted for 30 January, and closing on 6 February.

-

Market softening likely to being in 2025 as new capital is tempted in.

-

The investment firm said cat bond spreads that are elevated relative to historical levels continue to offer an attractive entry point for investors.

-

Pricing on Class A notes has reduced for a second time.

-

The sidecars segment has been attracting inflows after returns hit a high note in 2023.

-

The health insurer now expects to secure the lowest-risk tranche of its health bond for under a 3% spread.

-

The Seaside Re placement is the first cat bond lite deal of 2024.

-

Allstate has expanded the size of the bond twice, now reaching $400mn.

-

In total nearly $139mn worth of bonds have been extended.

-

The deal was brokered by Gallagher Re and provides US cyber insurance event protection.

-

The early redemption of the Credit Suisse bond comes after the bank was acquired by its rival UBS last year.

-

In its semi-annual report for the six months to 31 July 2023, the manager said the fund had returned 2.74% over the half-year.

-

Earlier today, the insurer updated the spread on the cat bond which has settled at 5.75%, and updated the target price to $300mn-$350mn.

-

Allstate increased the target size of the bond to $300mn-$350mn, up from $200mn.

-

The bond will provide protection from named storms in Florida for three years.

-

Insurance competition remains vibrant in some of the segments that remain most exposed to persistent risks highlighted by the flagship World Economic Forum report.

-

The independent manager’s post-Ian growth has helped it more than double from prior estimated assets under management.

-

The carrier is seeking indemnity per occurrence for quake coverage in the US.

-

The Swiss Re Total Return Index climbed month-over-month throughout the year, to more than regain ground lost after Hurricane Ian in September 2022.

-

Nearly 90% of the fund’s allocation is in cat bonds, with a small allocation to other ILS securities and US Treasury Bills.

-

-

The firm will deploy newly developed, proprietary cat bond analysis platform Hubble.

-

Roughly $750mn of securities across 13 cells are available to institutional investors via London Bridge vehicles.

-

The performance continues an unbroken run of positive monthly returns in 2023.

-

Broker-dealers' year-ahead forecasts have undershot total final issuance in three of the last five years.

-

Steiger will oversee the new article 8 classified fund, based out of Zurich.

-

While it is too early to determine the total financial loss, the US Geological Survey believes there is a 64% likelihood it will reach into the billions of US dollars.

-

The $7bn initial attachment point has remained unchanged from last year.

-

The new fund generated 11.2% in profits for the period from 27 January to 31 October last year.

Most Recent